Redlining facts for kids

Redlining is an unfair practice where important services, like home loans or insurance, are made difficult or impossible to get for people living in certain neighborhoods. This often happened in areas where many racial and ethnic minority groups lived. It was very common in the United States, especially affecting African Americans, Mexican Americans, Jewish Americans, and Italian Americans.

For example, people in redlined areas might have been denied loans to buy or fix homes, couldn't get insurance, or found it hard to access good healthcare. Sometimes, these areas even became "food deserts," meaning there were few stores selling fresh, healthy food.

Reverse redlining is another unfair practice. It happens when lenders or insurance companies specifically target neighborhoods with many minority residents. They might offer loans or services with much higher costs or unfair terms, knowing that people in these areas have fewer other choices. This took advantage of the lack of fair competition.

The term "redlining" was first used in the 1960s by a sociologist named John McKnight. He described how banks in Chicago, Illinois drew red lines on maps around neighborhoods they considered "hazardous." This meant they wouldn't invest in these areas, often because of the racial background of the people living there. Later, in the 1980s, a reporter named Bill Dedman showed how banks in Atlanta would lend money in lower-income white neighborhoods but not in Black neighborhoods, even if those Black neighborhoods had higher incomes.

Redlining is a clear example of how systemic racism has affected American society. It led to unfair differences in education and housing between different racial groups. It also created spatial inequality, meaning unequal opportunities based on where people lived, and economic inequality, leading to differences in wealth.

Contents

How Redlining Started

Redlining in the United States grew out of a history of separating people by race and treating minority groups unfairly. It began with real estate sales practices and ideas about how race affected property values.

The federal government became involved with the National Housing Act of 1934. This law helped create the Federal Housing Administration (FHA). The FHA developed a formal system for redlining. They created rules for giving out home loans. This federal policy made it harder for minority neighborhoods in cities to get money for homes. This led to these areas becoming neglected and isolated. The unfair ideas behind redlining made racial segregation and urban decay worse in the United States.

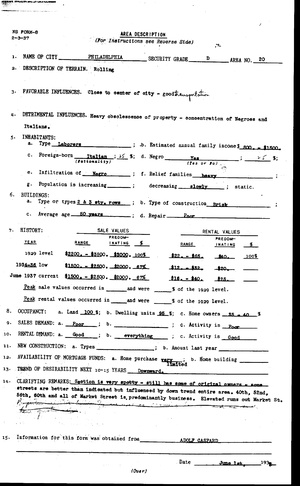

In 1935, the Home Owners' Loan Corporation (HOLC) created "residential security maps" for many cities. These maps showed how safe it was to invest in real estate in different areas.

- Green areas (Type A) were the newest and most desirable for loans, often wealthy suburbs.

- Blue areas (Type B) were "Still Desirable."

- Yellow areas (Type C) were "Declining."

- Red areas (Type D) were considered the riskiest for home loans. These "redlined" neighborhoods were often older city districts. They included most African-American households, even though about 85% of residents in these areas were white. Only a few majority African-American neighborhoods were not rated "Type D."

These maps were used by both private companies and the government for many years. They made it difficult for people in Black communities to get loans. The FHA's rules even told banks to avoid areas with "different racial groups." Between 1945 and 1959, African Americans received less than 2% of all home loans that the federal government insured.

Property insurance companies also used redlining after World War II. They often refused to offer comprehensive homeowners' insurance in neighborhoods where people of color lived. One insurance company even advised its workers to "use a red line around questionable areas on territorial maps."

In the 1970s, community groups in Chicago, led by people like Gale Cincotta, started fighting against redlining. They formed the National People's Action (NPA) to demand that banks reveal their lending patterns. These groups worked to show how banks were unfairly refusing to invest in certain neighborhoods.

Efforts to End Redlining

Important Laws Against Discrimination

The United States government passed several important laws to stop redlining and other unfair practices:

- The Fair Housing Act of 1968 made it illegal to discriminate in housing based on race or national origin. This meant it was against the law to refuse to sell or rent a home, or to offer different terms, because of someone's background. The Office of Fair Housing and Equal Opportunity helps enforce this law.

- The Equal Credit Opportunity Act (ECOA), passed in 1974, made it illegal for any lender to discriminate against someone applying for credit. This includes discrimination based on race, color, religion, national origin, sex, marital status, or age.

- The Community Reinvestment Act (CRA), passed in 1977, requires banks to lend money fairly in all communities, including low- and moderate-income areas.

Community Action and Change

Community groups played a big role in fighting redlining. For example, ShoreBank in Chicago was a special bank founded in 1973. It aimed to help African-American communities get financial services and home loans, fighting against unfair lending.

In the mid-1970s, groups like the South Austin Coalition Community Council (SACCC) in Illinois also worked to restore their neighborhoods. They fought against financial institutions that were accused of redlining. Their efforts helped bring attention to these issues and led to new laws.

Redlining's Lasting Impact Today

Even though redlining is illegal, its effects can still be seen in many American cities today.

Neighborhood Segregation

Many cities still have neighborhoods that are largely separated by race. Cities like Chicago, Detroit, Houston, and Atlanta show clear boundaries between Black and white neighborhoods. These are often the same areas that were redlined decades ago. This continued separation can make it harder for millions of people to improve their economic situation.

Unfair Property Rules

In the past, many property deeds had "racial covenants." These were rules that said only certain racial groups could live in a house or neighborhood. The Supreme Court made these rules "unenforceable" in 1948, meaning courts couldn't make people follow them. But it wasn't until the Fair Housing Act of 1968 that they became truly illegal.

Today, states like California, Washington, and Minnesota have passed laws to help remove these old, unfair rules from property records. Projects like "Mapping Prejudice" also help people learn about and understand the history of these covenants.

The Wealth Gap

Redlining greatly contributed to what is now called the Racial Wealth Gap. This is the difference in how much wealth (like savings, homes, and investments) different racial groups have.

- Neighborhoods that were redlined in the 1930s often still have lower home values and fewer homeowners today.

- It has been harder for Black families to build wealth over generations. Studies show that Black children born into lower-income families have a much smaller chance of moving into higher-income groups compared to white children.

- Because many African Americans couldn't get fair home loans, they sometimes had to turn to lenders who charged very high interest rates. This made it harder to own homes and build wealth.

Unfair Financial Services

Redlining also led to unfair practices in other financial services:

- Student Loans: In 2007, a group lawsuit was filed against a student loan company, Sallie Mae. It claimed the company unfairly affected African American and Hispanic students with its loan terms. The case was settled in 2011.

- Credit Cards: Some credit card companies have been accused of "digital redlining." This means they might offer different amounts of credit to people in certain areas based on their ethnic background, rather than just their financial history.

- Banks: Banks sometimes denied loans or offered stricter repayment terms to people from redlined areas. This made it very difficult for African Americans to own homes.

- Insurance: Even today, race can affect how insurance companies set policies and rates. Some companies have been accused of using maps and demographic data to charge higher rates in certain ZIP codes.

- Mortgages: In "reverse redlining," lenders targeted minority communities with expensive and unfair loans, known as "subprime mortgages." These loans often had very high interest rates and fees, trapping homeowners in debt and sometimes causing them to lose their homes. Major banks like Wells Fargo, Bank of America, and JPMorgan Chase have settled lawsuits for discriminatory lending practices against African-American and Hispanic borrowers.

Environmental Racism

Historically redlined communities often face "environmental racism." This means they are more likely to have:

- Smaller, less accessible, or poorer quality parks.

- Higher levels of air pollution, like nitrogen dioxide and fine particles, which can lead to health problems like heart and lung diseases.

- More facilities that produce hazardous waste. For example, studies in 2022 found that redlined areas in 202 US cities had higher air pollution levels.

These environmental issues can have a direct impact on public health.

Digital Redlining

"Digital redlining" is a modern form of discrimination using technology. It involves creating unfair differences between groups through digital tools, online content, and the internet. For example, in 2019, the United States Department of Housing and Urban Development (HUD) charged Facebook with housing discrimination. They said Facebook allowed advertisers to exclude certain groups of people from seeing housing ads, based on things like their background or interests.

Health Inequality

Redlining and other forms of unfair treatment still affect people's health today. Neighborhoods that were redlined often have higher rates of illnesses like diabetes, heart disease, and high blood pressure. This is because people in these areas might have limited access to good housing, healthy foods, and medical care.

- Studies show that women in historically redlined areas have a higher chance of giving birth too early.

- Life Expectancy: People in historically redlined communities often have lower life expectancies. On average, life expectancy in redlined communities is 3.6 years lower than in highly rated neighborhoods. In some cities, this difference can be even greater.

- COVID-19: The effects of redlining were also seen during the COVID-19 pandemic. Areas that were redlined in the 1930s were often the same neighborhoods most affected by the virus. This was due to factors like concentrated poverty, limited healthcare access, and crowded living conditions, all linked to the long-term impacts of redlining.

Ways to Fix Redlining's Effects

To help communities recover from redlining, several strategies are important:

- Targeted Investments: Directing resources to improve jobs, incomes, housing, and social services in struggling communities.

- Better Transportation: Recognizing that good public transportation helps people in low-income areas get to jobs and services.

- Economic Development: Creating jobs close to where people live.

- Housing Improvement: Investing in homes and neighborhoods through revitalization programs.

- Fair Zoning: Using rules like "inclusionary zoning" to ensure there's enough good quality housing for everyone.

- Environmental Justice: Making sure that hazardous waste sites are not unfairly concentrated in low-income and minority areas.

Healthcare professionals also have a role to play. They can learn about how historical injustices like redlining affect their patients' health. By understanding these larger issues, healthcare providers can better support communities and work towards fairer health outcomes for all.

See also

In Spanish: Redlining para niños

In Spanish: Redlining para niños

- Housing segregation

- Gentrification in the United States

- Ghetto tax

- Racial capitalism

- Sundown town