Economic history of the Republic of Ireland facts for kids

The economic history of the Republic of Ireland began in 1922. This was when the Irish Free State became independent from the United Kingdom. For many years, the country faced poverty and many people left to find work elsewhere.

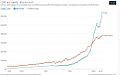

However, things started to get better in the 1960s. But then, in the 1970s and 1980s, economic problems returned, and more people left Ireland. The 1990s brought a huge change, with a period of amazing economic growth known as the "Celtic Tiger". This success lasted until the global financial crisis in 2008.

After the crisis, Ireland faced tough times and became very indebted. But by 2015, the country started growing again, becoming one of the fastest-growing economies. By 2017, unemployment was at its lowest in nine years. Experts like Kevin O'Rourke believe that Ireland's independence and joining the European Union were key to its economic success.

Contents

How Independence Changed Ireland's Economy

After the Irish War of Independence, 26 counties of Ireland became independent. They formed the Irish Free State, a dominion of the UK. The other six counties in the northeast remained part of the UK, forming Northern Ireland. In 1937, the Irish Free State changed its name to Ireland, which is its name today.

There was already an economic difference between the north and the rest of Ireland. After the country was divided, these differences grew even more. For example, County Donegal was cut off from its main trading city, Derry, which was now in Northern Ireland. The railway network also struggled to work across the new border.

Despite these challenges, some believe that the division of Ireland had only a small effect on the economy overall. The new Irish Free State had the power to control its own money and taxes. However, the fighting from 1919 to 1923 caused a lot of economic damage. The new state started with a large budget problem that took until 1931 to fix.

Building the Economy (1922-1960s)

When the Irish Free State was set up, it was the first real effort to build industries in the south of Ireland since the 1890s. The country had limited money and resources. Farming changed from growing crops to raising animals, with more focus on processing products and exporting them.

Ireland slowly got electricity, and new state-owned factories were encouraged. One example was the Irish Sugar Company in Carlow. During the 1930s, Ireland was mostly a farming country that traded mainly with the UK. It exported mostly beef and dairy products.

In the late 1930s, the government had a serious disagreement with Britain over payments for land. This was called The Economic War. Ireland refused to pay, so Britain put taxes on Irish beef. Ireland responded by taxing British goods. This "economic war" ended in 1938.

From 1932, Éamon de Valera's government stopped free trade. They tried to protect Irish industries and make the country self-sufficient. But Ireland wasn't rich enough for this plan to work well. The government took control of many private businesses, turning them into state-owned companies. Some of these companies are still partly owned by the state today. Others were sold or closed later when they weren't making enough money.

The Booming 1960s

The 1960s saw a big growth in Ireland's economy, led by Seán Lemass. Many housing projects began, like in Ballymun, to replace old, crowded housing in Dublin. The Industrial Development Authority started focusing on high-tech industries. They also encouraged companies from other countries to invest in Ireland.

Education also changed a lot. The state built new technical colleges and higher education institutes. These greatly expanded learning, especially in technical skills. University education also improved and grew. When Ireland joined the European Economic Community (now the European Union) in 1973, it further boosted Ireland's economic future. Before this, 90% of Ireland's exports went to Britain.

Some historians, like Professor Tom Garvin, have pointed out that while Lemass is praised for opening up trade after 1960, he was also the one who supported protectionism from 1932.

A report in 1968, known as the Buchanan Report, looked at how to plan for economic growth in different regions of Ireland. It suggested having a few main development centers. However, local politics often led to industries being spread out, which was not as effective.

Challenges in the 1970s and 1980s

In the 1970s, Ireland joined the European Economic Community, which helped the country start to catch up with the rest of Europe. However, this good period didn't last long. There were many worker strikes, and prices went up a lot because of oil crises in 1973 and 1979. Poor management of the economy by the government also caused problems. By the 1980s, Ireland was sometimes called the 'sick man of Europe'.

The 1980s were a very difficult time for Ireland. A government budget in 1977, which included removing car tax and borrowing money for everyday spending, combined with global economic issues, hurt the Irish economy for most of the 1980s. This led to high unemployment and many people leaving the country.

Governments led by Charles Haughey and Garret FitzGerald made things worse by borrowing even more money. Tax rates were very high, sometimes as much as 60%. Ireland also had an overvalued currency for much of the 1980s, which meant its money was worth too much compared to other currencies. This made Irish exports expensive and hurt trade.

This was also a time of political instability, with governments often not lasting long. The problems began to be fixed in 1987. The government started economic reforms, cut taxes, changed welfare, and reduced borrowing. Support from the European Union was a big help during this time.

The "Celtic Tiger" (1995–2007)

In the 1990s, Ireland's economy entered its "Celtic Tiger" phase. This was a time of amazing growth. Many foreign companies invested in Ireland, thanks to a low company tax rate. Better economic management and a new way of working together between businesses and workers also helped. The European Union invested over €10 billion in improving Ireland's roads and other important structures.

By 2000, Ireland had become one of the richest countries in the world. Unemployment was very low, at 4%, and income tax rates were almost half of what they were in the 1980s. During this time, Ireland's economy grew by five to six percent each year. This dramatically increased people's incomes, making them equal to and even higher than those in many other Western European countries.

The Irish government worked to control rising prices, lower taxes, and reduce government spending. They also focused on improving workers' skills and encouraging foreign investment. Ireland joined eleven other European Union countries in using the euro currency in January 1999. The economy did slow down a bit after 2001, especially in the high-tech export sector. However, overall economic growth remained strong for a few more years.

Images for kids

-

The Irish pound (Punt) served as the Republic's currency from 1979 until 2002.

-

Historical GDP per capita development of Ireland and the UK

.png)