Central Bank of Ireland facts for kids

-_ALONG_BOTANIC_AVENUE_(JANUARY_2018)-135336_(27856978779).jpg) |

|

| Headquarters |

|

|---|---|

| Established | 1 February 1943 |

| Ownership | 100% state ownership |

| Governor | Gabriel Makhlouf (since September 2019) |

| Central bank of | Ireland |

| Reserves | 740 million USD |

| Preceded by | Currency Commission (currency control) Bank of Ireland (Government's banker)1 |

| 1 Even after establishment of the Central Bank, the Bank of Ireland remained the government's banker until 1 January 1972. 2 The Central Bank of Ireland still exists but many functions have been taken over by the ECB. |

|

The Central Bank of Ireland (Irish: Banc Ceannais na hÉireann) is like Ireland's main financial helper. It's part of the Eurosystem, which manages the Euro currency for many European countries. From 1943 to 1998, it was in charge of Ireland's money, the Irish pound. Today, it also makes sure that banks and other financial companies in Ireland follow the rules. Since 2014, it has been Ireland's main authority for European Banking Supervision.

The Central Bank of Ireland started on 1 February 1943. Since 1972, it has also been the main bank for the Government of Ireland. This change made it a full central bank, not just a currency board.

Its main office was on Dame Street, Dublin, from 1979 to 2017. Since March 2017, its headquarters are on North Wall Quay. Here, people can exchange old Irish money for Euros. They can also exchange large Euro banknotes or damaged money. The bank also has offices at Spencer Dock. The Currency Centre in Sandyford is where the bank makes, stores, and sends out money.

Contents

History of Ireland's Money

When the Irish Free State became independent in 1922, most of its trade was with the United Kingdom. So, creating a new Irish currency was not the top priority. British banknotes and coins were still used in Ireland. Irish banks also issued their own notes.

In 1926, the government started making its own coins. These coins were similar to British ones. They began circulating on 12 December 1928.

In 1927, a new Irish currency unit was created. It was called the Saorstát Pound (Free State Pound). This new pound was kept at the same value as the British Pound Sterling. A special group called the Currency Commission made sure of this. They held British government money and gold to keep the values equal.

From 1928 to 1979, the UK and Ireland had a de facto currency union. This means their currencies were basically linked.

The Central Bank Act 1942 officially changed the Currency Commission's name. On 1 February 1943, it became the Central Bank of Ireland. However, it wasn't yet a full central bank. For example, it didn't hold the cash reserves of other banks. It also couldn't easily control how much money was available. The Bank of Ireland also remained the government's main bank for a while.

Over many years, the Central Bank slowly took on more duties. But it mostly acted like a currency board until the 1970s.

In 1978, European leaders decided to create a "zone of monetary stability." This led to the European Monetary System (EMS). The EMS aimed to keep exchange rates stable between European currencies. It also created the ECU, which was a mix of different European currencies. The ECU was a step towards the Euro.

On 15 December 1978, Ireland announced it would join the EMS. The EMS started on 13 March 1979. Soon after, the British Pound Sterling started to get stronger. This was due to rising oil prices. By 30 March, the Irish currency could no longer stay linked to the British Pound. After over 50 years, the link between Irish and British money was broken. The Irish currency then became known as the Irish pound (or Punt in Irish).

At first, joining the EMS was a bit difficult for Ireland. It was hoped the Irish Pound would get stronger. This would help reduce price increases (inflation) in Ireland. But the British Pound became much stronger. This was partly because Britain had a lot of oil. By late 1980, the Irish Pound was worth less than 80 British pence. Inflation in Ireland was also higher than in Britain.

Eventually, the EMS became more stable. The Irish Pound was devalued by 10% in 1992. But from 1987 onwards, Ireland's inflation rate was similar to or lower than Britain's.

Journey to the Euro

The idea of a single European currency started way back in 1950. Plans for how to create this currency were made over the years. The Delors Report in 1989 suggested a three-step plan. This plan became law with the Maastricht Treaty in 1992. In Ireland, people voted on this treaty in a referendum in June 1992. About 70% of voters said yes.

The treaty planned for monetary union to begin on 1 January 1999. New Euro notes and coins would be introduced on 1 January 2002.

The Central Bank of Ireland began making Euro coins in September 1999. They made over a billion coins at the Currency Centre in Sandyford. These coins weighed about 5,000 tons. Their total value was €230 million. Euro coins started being used in January 2002. The bank also started printing Euro banknotes in June 2000. They printed 300 million notes worth €4 billion. These notes were in denominations of 5, 10, 20, 50, and 100 euros. Euro banknotes made for the Central Bank have a serial number starting with the letter T.

What the Central Bank Does

The Central Bank of Ireland has many important jobs. These jobs help the people of Ireland and Europe. Some of its main responsibilities include:

- Keeping prices stable: This means making sure prices don't go up too quickly.

- Keeping the financial system stable: This means making sure banks and other money businesses are safe.

- Protecting customers: Making sure people are treated fairly by financial companies.

- Checking and enforcing rules: Making sure financial companies follow the laws.

- Developing new rules: Creating policies for how financial businesses should operate.

- Managing payment systems: Making sure money can be moved safely and quickly.

- Giving economic advice: Helping the government make good financial decisions.

- Collecting financial statistics: Gathering data about the economy.

- Helping struggling financial companies: Working to fix problems if a financial company is in trouble.

Governors of the Central Bank

The Governor is the head of the Central Bank. The President of Ireland appoints the Governor. This is done based on advice from the Government of Ireland.

| Name (Birth–Death) |

Term of office |

|---|---|

| Joseph Brennan (1887–1963) |

1943–1953 |

| James J. McElligott (1890–1974) |

1953–1960 |

| Maurice Moynihan (1902–1999) |

1960–1969 |

| T. K. Whitaker (1916–2017) |

1969–1976 |

| Charles Henry Murray (1917–2008) |

1976–1981 |

| Tomás F. Ó Cofaigh (1921–2015) |

1981–1987 |

| Maurice F. Doyle (1932–2009) |

1987–1994 |

| Maurice O'Connell (1936–2019) |

1994–2002 |

| John Hurley (1945 – ) |

2002–2009 |

| Patrick Honohan (1949 – ) |

2009–2015 |

| Philip R. Lane (1969 – ) |

2015–2019 |

| Gabriel Makhlouf (1960 – ) |

2019–Present |

More Pictures

-

In 2016, former Irish Finance Minister Michael Noonan spoke about Ireland's tax policies.

-

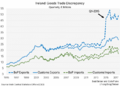

This chart shows differences in trade figures for Ireland.

-

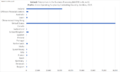

Dominance of U.S. companies: This chart shows profits of companies in Ireland, based on where their main owners are from.

-

This chart compares office building prices in Dublin to other EU countries.

-

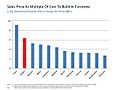

This chart compares the sales price of prime offices in Dublin to other EU countries.

.jpg)

.png)

.jpg)

.jpg)

See also

In Spanish: Banco Central de Irlanda para niños

In Spanish: Banco Central de Irlanda para niños

- Banknotes of the Republic of Ireland

- Coins of Ireland

- Economy of the Republic of Ireland

- Irish pound

- Irish modified GNI (or GNI star)

- Irish Fiscal Advisory Council

- Green Jersey Agenda

- Ireland as a tax haven

- List of central banks