Supply and demand facts for kids

Supply and demand is a basic idea in microeconomics, which is the study of how people and businesses make decisions. It helps us understand how the price of something is decided in a market economy. There are two main parts to this idea:

- Supply: This is how much of a product or service is available.

- Demand: This is how much of that product or service people want to buy.

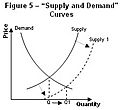

Supply and demand show how producers (the people who make things) and consumers (the people who buy things) work together. This relationship helps set the price for different goods. In a market where there is a lot of competition, the amount people want (demand) and the amount available (supply) will become equal. When this happens, the price is set, and we call it an economic equilibrium.

Contents

How Supply and Demand Change Prices

For most everyday items and markets, there are four main rules that explain how prices change when supply or demand shifts:

- If more people want something (demand increases) but the amount available stays the same (supply stays the same), there will be a shortage. This means the price will go up.

- If fewer people want something (demand decreases) but the amount available stays the same (supply stays the same), there will be a surplus. This means the price will go down.

- If more of something becomes available (supply increases) but the number of people who want it stays the same (demand stays the same), there will be a surplus. This means the price will go down.

- If less of something becomes available (supply decreases) but the number of people who want it stays the same (demand stays the same), there will be a shortage. This means the price will go up.

When there is a lot of something available, prices usually fall. This is because people do not want to pay a lot for items they can easily find. But when many people want to buy the same item and there isn't enough of it, prices will go up.

When people start wanting new goods and services, new markets often appear. The more people want something, the faster this happens. As more companies start making these items, the supply goes up. This increased supply then pushes the price down closer to the actual cost of making and selling the item.

Who Discovered Supply and Demand?

One of the first thinkers to notice these ideas was Adam Smith. In his famous book, The Wealth of Nations (published in 1776), he wrote that how much people wanted a good depended on its price. However, he didn't fully explain that demand also affects the price.

Later, David Ricardo published his book Principles of Political Economy and Taxation in 1817. In this book, he explained how market equilibrium works, much like we understand it today. Other important people who helped develop this model include Alfred Marshall and Léon Walras.

When the Rules Are Different

Sometimes, the usual rules of supply and demand don't quite fit. Here are a few examples:

- Giffen goods: These are rare items where people actually buy more of them if their price goes up. This usually happens when the price of a better, more expensive item also rises.

- Luxury goods (Veblen goods): Some people buy certain goods just to show off their wealth. This is called conspicuous consumption. For these items, like very expensive cars or jewelry, demand might go up when the price goes up, because the high price itself makes them seem more special.

- Snob effect: This happens when rich people buy less of a certain good if people with less money start buying it. They might want to keep their purchases unique.

The basic rules of supply and demand work best in a market with perfect competition. In such a market, there are many buyers and sellers, and no single person or company can control the price.

What if There's Only One Seller or Buyer?

- Monopoly: If there is only one supplier for a product (a monopoly), that supplier can choose the price. The demand then only decides how much people will buy at that price. The supplier will likely set a very high price as long as people are still willing to buy it.

- Monopsony: If there is only one buyer for a product, the market is called a monopsony. In this case, the single buyer can often set the price they are willing to pay.

Images for kids

-

Supply and demand curves

-

Adam Smith

See also

In Spanish: Oferta y demanda para niños

In Spanish: Oferta y demanda para niños